How Policy Prices Emissions – #2b

How Policy Prices Emissions – #2b

Powerful pressure, or pitiful pittance?

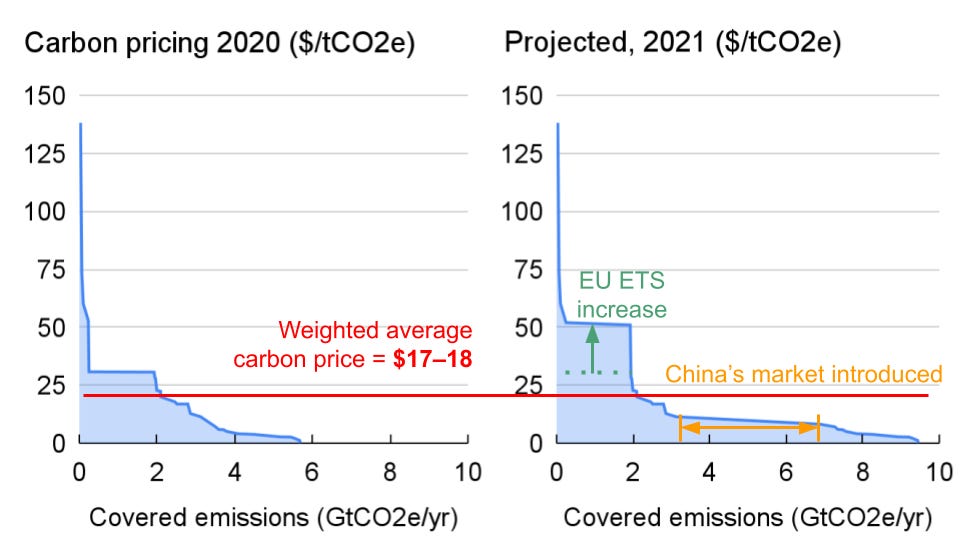

The weighted average price on emissions from 2020 policies was $17–18/tCO2. Although the EU’s ETS is making headlines with record-high prices, China’s new carbon market covers nearly 4 billion tons at a measly $8/tCO2. The combined effect of these two major market changes in 2021? Nothing – from the global weighted average carbon price perspective.

Although I’ve chosen the global weighted average carbon price as my metric of measure, you may see the logical pitfall. Global policy coverage with low carbon prices don’t move the needle on emission elimination. Serious decarbonization only occurs when the price is powerful enough to affect change. The solution is not ‘A price on carbon’, but ‘an Appropriate price on carbon’.

China’s carbon pricing is currently a pittance, but remember – the EU ETS was also pitifully powerless in driving decarbonization prior to 2018.

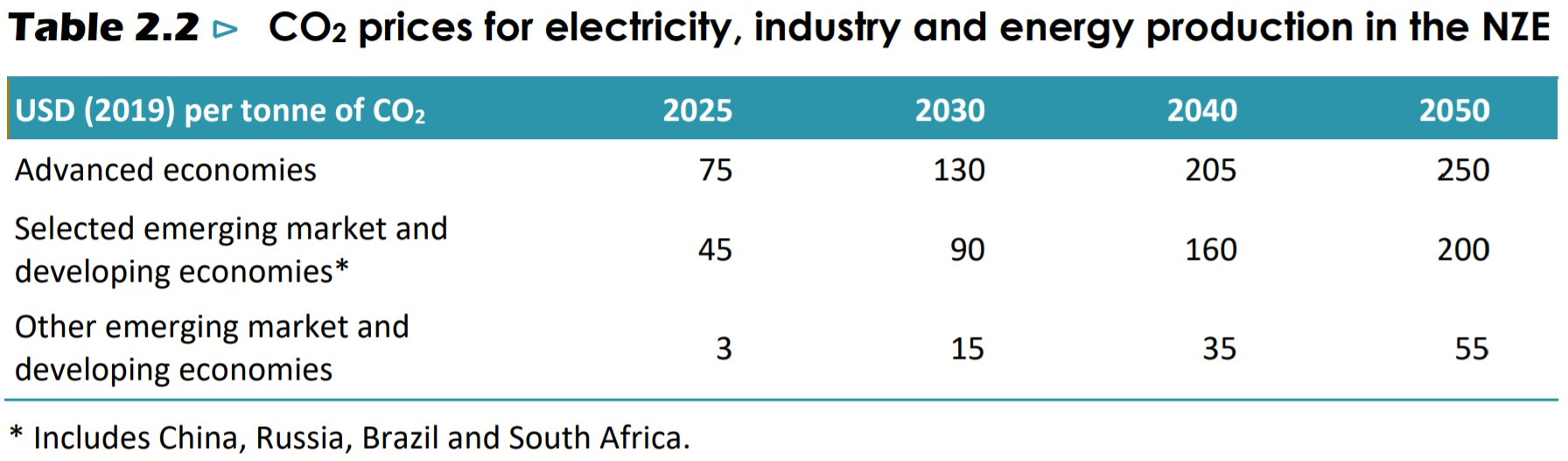

An ‘appropriate’ carbon price is not one size fits all. The IEA’s recent net-zero by 2050 modeling exercise described what might be considered a benchmark goal for carbon pricing around the world.

If China’s carbon market doesn’t strengthen to the ~$45/t level by 2025, it’s potency will remain questionable. If the U.S. doesn’t have nationwide carrots and sticks pricing carbon at $130/t by 2030, decarbonization will continue to be insufficient.

Simply put: if we fall short of these prices, we are less likely to hit net-zero by 20501.

When will the U.S. become an Advanced economy?

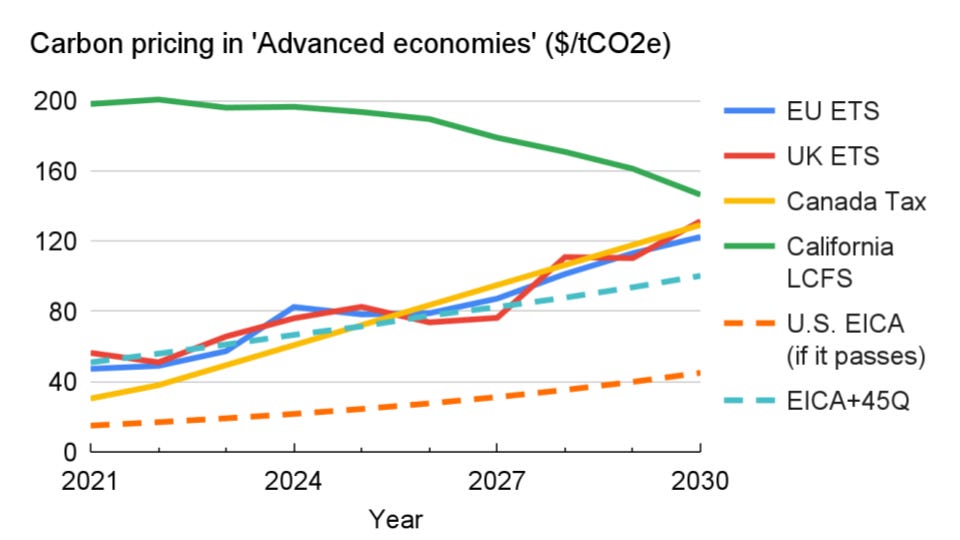

The last post briefly highlighted the United States’ reluctance to set a carbon price. For what it’s worth, there are a handful of bills with bipartisan support awaiting Congress. One, the Energy Innovation Act, has broad support boasting 79 co-sponsors. Before you get too excited, it’s important to note these prices are mostly aligned with the IEA’s ‘Selected emerging market and developing economies’, not the ‘Advanced economies’2.

What’s missing from the U.S. carbon pricing ‘stick’ data is a slew of other policies that provide ‘carrots’. Section 45Q of the U.S. tax code offers roughly $50/tCO2 for carbon capture and storage from air or point sources. Combine that incentive with the Energy Innovation Act disincentive and the U.S. becomes aligned with the IEA’s target carbon price for ‘Advanced economies’ in 2025. What’s more, the U.S. is working on several other incentives and tax credits to subsidize decarbonization3.

Prices in the EU, UK and Canada seem roughly aligned with the ‘Advanced economies’ tract, and will likely subject 2GtCO2/yr (or more) of emissions to carbon prices exceeding $120/tCO2 by 2030. California’s Low Carbon Fuel Standard (LCFS) is also an oft-quoted program supporting decarbonization and carbon removal. It’s maintained a price near its $200/tCO2 cap for months. However, since the LCFS is tied to the state’s transport emissions, and California is rapidly electrifying, the value might fall as electric vehicle adoption increases.

The true test for ‘an appropriate price on carbon’ comes down to decarbonization economics and regional effectiveness against emissions. Want to be even more Anticarbon?

Next time we will start exploring the cost of getting the world to net-zero GHGs. I’ll finally tie this all back to carbon removal with a global marginal abatement cost curve – you won’t want to miss it!

These carbon prices are to reach net-zero by 2050, and do not accurately value the social cost of emissions.

The IEA’s definition of ‘Advanced economy’ includes most of Europe, North America, and Australia. (Australia, Austria, Belgium, Canada, Chile, Colombia, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Israel, Italy, Japan, Korea, Latvia, Lithuania, Luxembourg, Mexico, Netherlands, New Zealand, Norway, Poland, Portugal, Slovak Republic, Slovenia, Spain, Sweden, Switzerland, Turkey, United Kingdom, United States, Bulgaria, Croatia, Cyprus, Malta and Romania)